The RBA cash rate hits 4.35% for the third consecutive hike, matching 2011 levels. This article examines duration risk and portfolio construction implications.

~ 7 min. read

By: Datt Capital

The Reserve Bank of Australia raised the cash rate to 4.35 per cent on 5 May 2026, the third consecutive hike this year. The decision fully unwinds last year's easing cycle and reflects a material pickup in inflation that continues to feed into price pressures in 2026.

The more consequential question for investors is not what this RBA interest rate decision costs borrowers this month. It is what the structure of this cycle means for how long rates stay elevated, and which businesses can withstand it.

The RBA now expects headline inflation to peak at 4.8 per cent in mid-2026, with underlying inflation remaining above 3 per cent until mid-2027, and only returning to the 2.5 per cent midpoint of the target band by mid-2028. To achieve that path, the RBA's forecasts assume the cash rate rises further to 4.7 per cent by the end of 2026.

The Board cited higher inflation stemming from the ongoing Middle East conflict, including second-round effects, with risks tilted to the upside. These added to inflationary pressures already arising from capacity constraints. The Board also noted that financial conditions are not as tight for the same level of the cash rate as was true a few years ago.

That last point matters and deserves scrutiny. The RBA is signalling it may need to push harder than a nominal rate comparison would suggest.

The Board was candid about the growth trade-off. GDP forecasts for 2026 were trimmed lower, with household consumption expected to take a hit from weaker real incomes as higher prices erode spending power. RBA Deputy Governor Andrew Hauser described the scenario where inflation accelerates even as growth weakens as a policy "nightmare," noting that supply constraints limit the economy's ability to absorb shocks.

This is the high-case scenario in practice: not a brief tightening correction, but a prolonged period of restrictive policy operating against a structurally constrained economy.

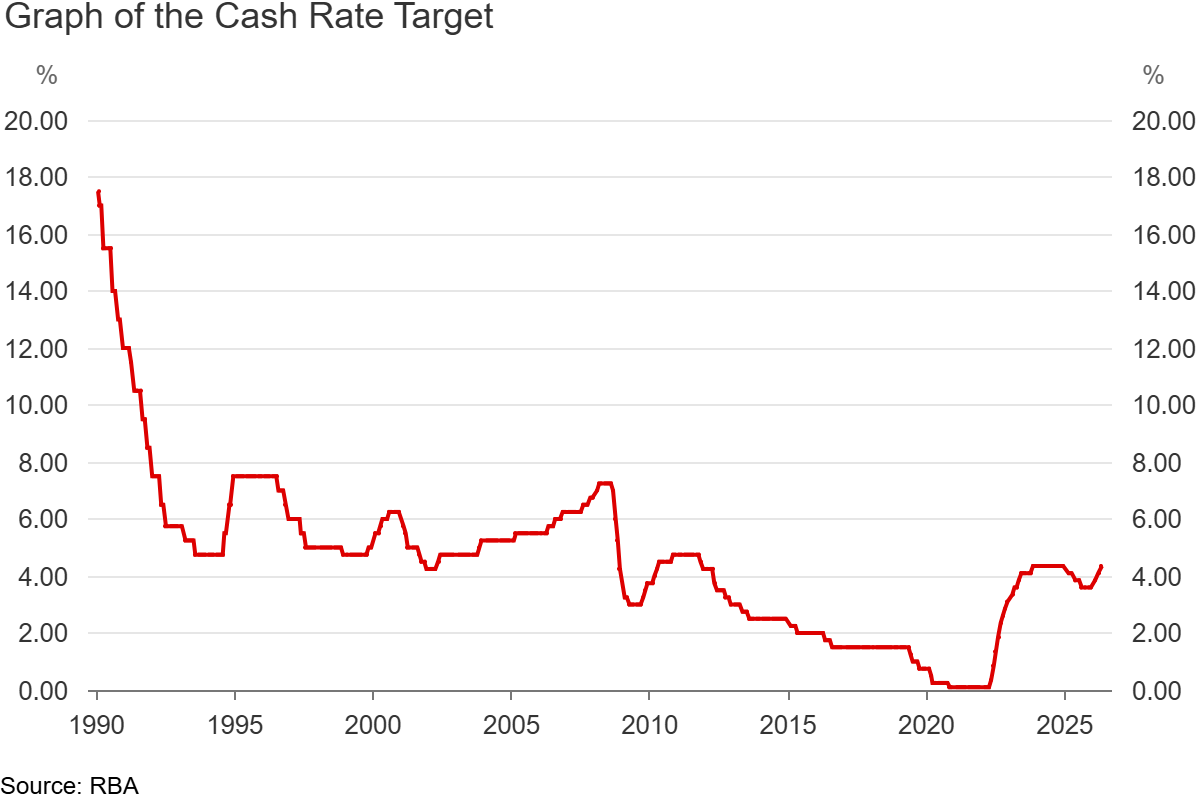

The cash rate is back at levels last seen in late 2011. That comparison is frequently cited. It is also frequently misread.

Graph of the RBA Cash Rate Target from 1990 to 2026, showing the cash rate at 4.35% in May 2026 following three consecutive hikes. Source: RBA.

There is a distinction that aggregate comparisons miss. In late 2011, the RBA was in an easing cycle. The cash rate had peaked and was moving lower, giving households and businesses a credible forward expectation of relief. Borrowing decisions, refinancing decisions, and investment decisions were all made against that backdrop.

In 2026, the direction is reversed. The RBA has signalled further hikes are possible, with market pricing pointing toward 4.7 per cent by year end and no cuts anticipated until 2028. Businesses and households are not pricing in relief. They are stress-testing against the possibility of more restriction. That asymmetry changes behaviour in ways that nominal rate comparisons do not capture.

The data reinforces this. Australian household debt to GDP reached approximately 113.7 per cent in mid-2025. The nominal mortgage balances being repriced today are far larger than in 2011, even at equivalent rates, because property prices have risen substantially in the intervening 15 years. Housing costs rose 6.5 per cent year-on-year to March 2026, and electricity prices are up 25 per cent as government rebates roll off. Households are absorbing rate increases on larger loan balances against a budget simultaneously compressed by structurally higher housing and energy costs. Roy Morgan modelling projects mortgage stress affecting 1.6 million Australians, approximately 30 per cent of borrowers, following the May hike.

Same rate on paper. Fundamentally different conditions underneath it.

The decision about whether the RBA hikes again is not the primary investment question. Markets have largely priced in further tightening. The more important question is duration: how long does the cash rate stay at or above 4.35 per cent?

The RBA's forecasts see underlying inflation remaining above 3 per cent until mid-2027, with the cash rate not expected to return toward neutral until 2028. That is a two-year window of restrictive monetary policy operating against elevated household debt, compressed discretionary budgets, and an economy growing at around 1.3 per cent annually. As we have written previously, interest rates are forcing discipline back into Australian small caps, and the duration of this cycle will determine which businesses emerge stronger.

In that environment, the investor's task is to distinguish between businesses that can absorb a sustained high-rate period and those whose earnings are structurally dependent on cheap credit or consumer discretionary spending.

Businesses positioned to absorb duration risk share common characteristics: low debt relative to earnings, high interest cover ratios, and pricing power that allows them to pass through input costs without losing volume. In the current cycle, energy producers and gold-linked businesses benefit directly from the inflationary conditions driving rates higher. We have examined the structural case for gold in a stagflationary environment and which ASX stocks face earnings downgrades from the energy shock in detail elsewhere. Defensive industrials and essential services with contracted revenue streams also carry structural insulation.

Businesses at risk in a prolonged high-rate environment include highly geared companies rolling over debt at materially higher rates than in prior years, consumer discretionary businesses exposed to the compression of household spending, and companies with thin margins in competitive industries where pricing power is limited. As covered in our sector analysis of RBA rate hike winners and losers, small-cap companies warrant particular scrutiny: while the segment contains businesses with strong earnings quality, the cohort as a whole carries higher refinancing risk and is more sensitive to credit tightening than large-cap peers.

Disciplined portfolio construction in this environment has to account for duration risk explicitly. Interest rate sensitivity in a bond portfolio favours floating-rate exposure over long-duration fixed instruments. In equities, it favours quality earnings over growth narratives that require continued multiple expansion.

Sequence of returns risk is also a material consideration in a sustained rate cycle. As we have outlined in our analysis of sequence of returns risk and the limits of average returns, a portfolio that absorbs a significant drawdown early in a high-rate period can take years to recover, even if average returns across the cycle appear acceptable. This is particularly relevant for investors in or approaching retirement.

A capital preservation strategy focused on risk-adjusted returns becomes more important, not less, as the cycle extends. Diversification across asset classes and geographies is more valuable in a period of domestic stagflation risk than in normal cycles, where correlation assumptions between asset classes hold more reliably. The Datt Capital Absolute Return Fund is structured around precisely this objective: generating positive risk-adjusted returns across the economic cycle, with capital preservation as a primary constraint rather than an afterthought.

Three consecutive hikes do not happen in isolation. They reflect a central bank that either miscalibrated its easing in 2025, or is now responding to an inflation shock partly outside its control, specifically the ongoing Middle East conflict and its energy price consequences.

The RBA stated it "will do what it considers necessary" to achieve price stability and full employment, and that having raised the cash rate three times, monetary policy is well placed to respond to further developments.

The signal is clear: the RBA is not yet confident the cycle is complete.

The investor decision is not about anticipating the next 25 basis points. It is about understanding that the economy is operating in a structurally different environment from the last period of equivalent nominal rates. Higher debt, higher housing costs, and persistent energy price inflation create a more restrictive transmission channel than the nominal comparison suggests.

Duration is the variable that matters. Which businesses can compound returns across a two-to-three year period of elevated rates? Which cannot? That distinction is where risk-adjusted returns are found in this cycle.

The RBA raised the cash rate to 4.35 per cent on 5 May 2026, marking the third consecutive hike in 2026.

The RBA's own forecasts project underlying inflation remaining above 3 per cent until mid-2027, with the cash rate expected to remain elevated through 2026 and into 2027. Rate cuts are not broadly anticipated until 2028.

While the nominal cash rate is comparable to 2011 levels, the RBA was cutting rates in late 2011, giving households and businesses a credible expectation of relief. In 2026, rates are rising with further hikes still possible. On top of the directional difference, Australian household debt is substantially larger in dollar terms, housing costs have risen significantly, and energy prices are adding compounding inflationary pressure.

Sectors with strong pricing power, low debt, and inelastic demand, such as energy, essential services, and quality defensive industrials, tend to be more resilient. Consumer discretionary businesses and highly leveraged companies face the most direct pressure.

Duration risk refers to a portfolio's sensitivity to changes in interest rates over time. In a high-rate environment, investors typically reduce exposure to long-duration fixed income and growth equities, and increase allocation to floating-rate instruments and businesses with stable, quality earnings.

An absolute return fund targets positive returns across different market conditions, rather than tracking a benchmark. In a sustained high-rate environment where traditional equity and bond portfolios face simultaneous pressure, an absolute return fund's focus on capital preservation and risk-adjusted returns can provide meaningful portfolio diversification.

Disclaimer: This article does not take into account your investment objectives, particular needs or financial situation; and should not be construed as advice in any way. The author may hold stocks discussed in this article. Forward-looking statements reflect the author's views at the time of writing and are subject to change. Past performance is not indicative of future results.

Investment Excellence with a Proven Edge

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2025. ALL RIGHTS RESERVED.

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2026. ALL RIGHTS RESERVED.

The information on this website is prepared and issued by Datt Capital Pty Ltd (ABN 37 124 330 865 AFSL 542100) (Datt Capital). Unless otherwise stated, the information is intended for wholesale clients within the meaning of section 761G or 761GA of the Corporations Act 2001 (Cth) (Corporations Act).

Datt Capital is the investment manager of the Datt Capital Absolute Return Fund (APIR FHT3309AU), the Datt Small Companies Fund Class A (APIR FHT4217AU), and the Datt Small Companies Fund Class B (APIR FHT4217AU) (together, the Funds). Fundhost Limited (ABN 69 092 517 087 AFSL 233045) (Fundhost) is the issuer and trustee of each Fund.

The Datt Capital Absolute Return Fund and the Datt Small Companies Fund Class A are available to wholesale investors only and must not be made available to any persons that are "retail clients" for the purpose of the Corporations Act. An investment in either of these Funds is available directly through a valid application form attached to the relevant information memorandum, through the Olivia123 direct application platform, or through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in either Fund you should consider the relevant information memorandum in full. The Datt Small Companies Fund Class B is available to retail investors only, exclusively through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in this Fund you should consider the relevant Product Disclosure Statement (PDS) in full. The PDS is available on request by contacting Datt Capital directly.

The information contained on this website or in any email is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Datt Capital or Fundhost to any registration or other requirement within such jurisdiction or country. Datt Capital may provide general information to help you understand our investment approach. Any financial advice we provide has not considered your personal circumstances and may not be suitable for you. To the extent permitted by law, Datt Capital and Fundhost, their officers, employees, consultants, advisers and authorised representatives, are not liable for any loss or damage arising as a result of any reliance placed on this document. Information has been obtained from sources believed to be reliable, but we do not represent it is accurate or complete, and it should not be relied upon as such. Datt Capital and Fundhost do not guarantee investment performance or distributions, and the value of your investment may rise or fall. Past performance is not an indicator of future performance.