Poor timing of losses can permanently damage a retirement portfolio. How the sequence of returns risk works and why capital preservation is the practical response.

~ 5 min. read

By: Datt Capital

Average returns are a flawed measure of investment success. They tell you nothing about the sequence in which those returns occurred, and for a retiree drawing down capital, sequence is everything.

This is particularly relevant when capital is being withdrawn. Two portfolios may report the same average return over a decade, yet deliver meaningfully different outcomes depending on when gains and losses occur. The path of returns, rather than the average itself, becomes the determining factor.

For investors focused on capital preservation, retirement income, and long-term wealth creation, this is a structural consideration that warrants close attention.

Sequence of returns risk refers to the impact that the order of investment returns has on a portfolio. It affects investors at every stage, but the consequences differ materially depending on whether capital is being accumulated or withdrawn.

During accumulation, early losses are less damaging. Contributions continue at lower prices, the capital base is smaller, and time allows for recovery. The investor effectively buys more units cheaply and benefits when markets recover.

However, during drawdown, the dynamic reverses. When negative returns occur at the point an investor begins withdrawing capital, they are required to fund their liquidity needs by selling assets at lower valuations. This reduces the capital base and limits participation in any subsequent recovery.

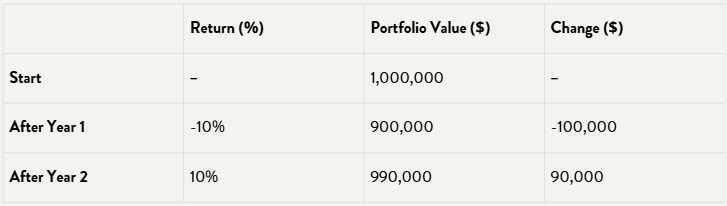

Average returns provide a simplified view of performance. They do not capture the dispersion of outcomes driven by volatility, drawdowns, or the timing of capital flows.

A portfolio that delivers alternating gains and losses may appear stable on an average basis. In practice, compounding is affected by the geometric progression of returns. Losses reduce the capital base from which future gains are generated.

For example, a 10% decline followed by a 10% gain does not restore the portfolio to its starting value. The recovery is incomplete because the gain is applied to a smaller base.

This dynamic becomes more pronounced as volatility increases. It reinforces the importance of managing drawdowns as part of the investment process.

Volatility drag reflects the difference between arithmetic and geometric returns. It is a fundamental driver of long-term outcomes.

As volatility increases, the compounding effect becomes less efficient. Larger drawdowns require disproportionately higher returns to recover. A 50% decline requires a 100% gain to return to the starting point. A 20% decline requires a 25% recovery.

These recovery mechanics shape portfolio construction. Limiting the depth and frequency of drawdowns supports a more consistent compounding profile over time.

From a capital allocation perspective, this is where risk asymmetry becomes important. Preserving capital during periods of market dislocation provides a stronger base for future returns.

In Australia, these dynamics are often observed within the small companies segment of the market.

This part of the market is characterised by lower liquidity, fragmented coverage, and a higher degree of mispricing. These conditions can create periods of significant dislocation, particularly when capital flows shift or when macro conditions tighten.

For investors, this presents both opportunity and risk. The opportunity arises from identifying undervalued companies with structural tailwinds and valuation support. The risk arises from participating in drawdowns that impair capital at the wrong point in the cycle.

A disciplined approach to security selection and position sizing is required to navigate this environment.

Consider an investor aged 57 with a portfolio valued at $950,000. The investor contributes $30,000 annually and plans to retire at 67.

Across two scenarios, the portfolio delivers an average return of 4.8% per annum over the period. The difference lies in the sequence of returns.

In the first scenario, negative returns are experienced earlier in the investment horizon. In the second scenario, those same negative returns occur later, closer to retirement.

Because this investor is still in the accumulation phase, contributing annually and not yet drawing down, early losses are less damaging. The capital base is smaller, contributions continue at lower prices, and there is time to recover.

The outcome diverges. The portfolio experiencing early losses reaches an ending value of approximately $1.95 million. The portfolio where losses occur later finishes at approximately $1.81 million. The difference is approximately $137,000.

This outcome is driven by two factors. The capital base is larger in later years, so drawdowns occur on a higher dollar value. There is also less time available for recovery before retirement.

The average return is unchanged. The sequence determines the result.

Disclaimer: This graph is provided for illustrative and educational purposes only. Past performance is not a reliable indicator of future performance.

The stakes change materially once withdrawals begin. Consider a retired investor aged 67 with a portfolio valued at $1,200,000. The investor withdraws $60,000 annually to fund living expenses.

Across two scenarios, the portfolio again delivers an average return of 4.8% per annum over a ten-year period. The difference is when the negative returns occur.

In the first scenario, significant negative returns occur in years one and two of retirement, at the point the portfolio is at its largest and withdrawals have just begun. In the second scenario, those same negative returns occur in years eight and nine.

The outcome diverges sharply. Early losses in retirement force the investor to sell assets at depressed prices to fund withdrawals. Those assets are no longer in the portfolio to participate in the recovery. Late losses, by contrast, occur on a portfolio that has already compounded for eight years and has a larger base to absorb them.

Unlike the accumulation example, there are no ongoing contributions to offset early losses. The damage is structural and, in many cases, permanent.

This is the mechanism that makes capital preservation a priority for investors in or approaching retirement. It is not about avoiding risk altogether. It is about avoiding the specific type of loss, early in drawdown, that cannot be recovered from.

Managing sequence of returns risk requires a focus on process rather than prediction.

At Datt Capital, this begins with an emphasis on capital preservation, liquidity, and valuation support. These factors influence how portfolios behave during periods of market stress. In practice, this involves investing with valuation support and strong balance sheets to limit downside, maintaining cash and liquidity to avoid forced selling, and allocating capital selectively when market dislocations present favourable risk-reward opportunities. Over time, these decisions shape the path of returns and reduce the risk of permanent capital impairment.

Cash is considered an active allocation. It provides optionality when market dislocations occur and reduces the likelihood of forced selling. This is particularly relevant in environments where liquidity can contract quickly. - says Emanuel Datt, CIO at Dat Capital

Portfolio construction also reflects a preference for idiosyncratic company drivers over broad macro narratives. This allows for a more granular assessment of risk and reduces reliance on market-wide movements.

In segments such as Australian small caps, where inefficiencies are more pronounced, this approach supports selective exposure to opportunities while maintaining capital discipline.

Sequence of returns risk highlights the importance of managing the path of returns alongside the level of return.

An absolute return framework focuses on preserving capital, limiting drawdowns, and compounding returns across different market conditions. The objective is to maintain a stable capital base that can participate in future opportunities.

For investors seeking a disciplined approach to capital preservation and risk management, the Datt Absolute Return Fund provides exposure to a strategy designed to manage drawdowns and compound capital across varying market conditions.

Long-term investment outcomes are shaped by more than average returns. The sequence in which returns occur, the depth of drawdowns, and the availability of liquidity all influence the end result.

Understanding these dynamics allows investors to better assess risk and structure portfolios with a greater degree of resilience.

For further detail on our investment philosophy and approach to managing risk and compounding capital, explore the Datt Absolute Return Fund.

Sequence of returns risk refers to the impact that the timing of investment returns has on a portfolio. It affects both accumulating and drawdown investors, but the consequences are most severe during the withdrawal phase, when selling depressed assets to fund living expenses can cause permanent capital impairment.

During accumulation, early losses are less damaging because contributions continue at lower prices and time allows for recovery. During drawdown, early losses are far more destructive. There are no contributions to offset them, assets must be sold at depressed prices to fund withdrawals, and the capital removed from the portfolio cannot participate in the subsequent recovery.

SMSF trustees in or approaching the pension phase are drawing down capital to fund retirement income. A significant market downturn early in retirement, when the portfolio is at its largest, can permanently reduce the capital base and shorten the life of the fund. Managing downside exposure in the years immediately before and after retirement is one of the most important decisions an SMSF trustee can make.

As investors approach retirement, the portfolio value is typically at its highest and withdrawals begin. Losses during this period affect a larger capital base and leave less time for recovery, which can materially reduce retirement outcomes.

Volatility reduces the efficiency of compounding. When a portfolio experiences drawdowns, future gains are applied to a smaller capital base. This creates a gap between average returns and actual investor outcomes over time.

Average returns do not reflect the path of returns, drawdowns, or timing of capital flows. Two portfolios with the same average return can produce different outcomes depending on when gains and losses occur.

Sequence risk can be managed through disciplined portfolio construction. This includes focusing on capital preservation, managing drawdowns, maintaining liquidity, and allocating to investments with strong valuation support and idiosyncratic drivers.

Disclaimer: This article does not take into account your investment objectives, particular needs or financial situation; and should not be construed as advice in any way. The author may hold stocks discussed in this article. Forward-looking statements reflect the author's views at the time of writing and are subject to change. Past performance is not indicative of future results.

Investment Excellence with a Proven Edge

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2025. ALL RIGHTS RESERVED.

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2026. ALL RIGHTS RESERVED.

The information on this website is prepared and issued by Datt Capital Pty Ltd (ABN 37 124 330 865 AFSL 542100) (Datt Capital). Unless otherwise stated, the information is intended for wholesale clients within the meaning of section 761G or 761GA of the Corporations Act 2001 (Cth) (Corporations Act).

Datt Capital is the investment manager of the Datt Capital Absolute Return Fund (APIR FHT3309AU), the Datt Small Companies Fund Class A (APIR FHT4217AU), and the Datt Small Companies Fund Class B (APIR FHT4217AU) (together, the Funds). Fundhost Limited (ABN 69 092 517 087 AFSL 233045) (Fundhost) is the issuer and trustee of each Fund.

The Datt Capital Absolute Return Fund and the Datt Small Companies Fund Class A are available to wholesale investors only and must not be made available to any persons that are "retail clients" for the purpose of the Corporations Act. An investment in either of these Funds is available directly through a valid application form attached to the relevant information memorandum, through the Olivia123 direct application platform, or through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in either Fund you should consider the relevant information memorandum in full. The Datt Small Companies Fund Class B is available to retail investors only, exclusively through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in this Fund you should consider the relevant Product Disclosure Statement (PDS) in full. The PDS is available on request by contacting Datt Capital directly.

The information contained on this website or in any email is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Datt Capital or Fundhost to any registration or other requirement within such jurisdiction or country. Datt Capital may provide general information to help you understand our investment approach. Any financial advice we provide has not considered your personal circumstances and may not be suitable for you. To the extent permitted by law, Datt Capital and Fundhost, their officers, employees, consultants, advisers and authorised representatives, are not liable for any loss or damage arising as a result of any reliance placed on this document. Information has been obtained from sources believed to be reliable, but we do not represent it is accurate or complete, and it should not be relied upon as such. Datt Capital and Fundhost do not guarantee investment performance or distributions, and the value of your investment may rise or fall. Past performance is not an indicator of future performance.