Learn how professional investors assess fund managers in Australia, including performance, drawdowns, fees, risk controls, governance, and due diligence questions to ask.

~ 4 min. read

By: Datt Capital

Australia’s investment landscape is moving quickly. Markets reprice, leadership changes, and different styles come in and out of favour. In that environment, selecting a fund manager is less about chasing what has worked recently and more about understanding how a manager makes decisions when conditions are uncertain.

That is why professional investors start with the fundamentals of the process. They do not choose a fund manager based on a good quarter or a strong 12-month chart. They know performance can be influenced by market conditions or a temporary style tailwind. So instead of focusing on recent returns alone, they run a structured due diligence process to understand what sits underneath the numbers.

This article breaks down how institutions and sophisticated allocators assess fund managers in Australia, what they measure, what they ask, and what makes an Australian investment manager investable at scale.

Professional manager selection typically runs in two tracks.

The goal is simple. Confirm the returns were earned through skill, within an intentional risk framework, and supported by a credible business structure.

Performance data is only the starting point. Investors test how the return was achieved and whether it is repeatable.

Net returns

Institutions focus on what investors receive after fees and costs. Gross returns are not investable. Net outcomes determine whether value-add is real.

Professionals check:

Risk-adjusted returns

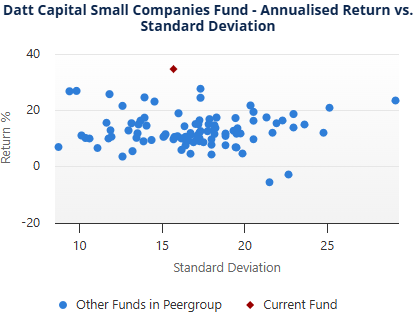

Two funds can deliver the same return with completely different risk taken. Professionals prefer controlled volatility and repeatable alpha sources.

Common metrics include:

Drawdowns and downside protection

Drawdowns are one of the strongest indicators of risk discipline. Institutional investors want to know how a manager behaves during stress.

They assess:

A manager who protects capital during stress improves long-term compounding outcomes.

Consistency across market cycles

Professionals avoid managers who only work in one regime. They test performance across multiple conditions to reduce timing risk.

They review:

Benchmark fit and peer comparison

Investors check whether performance is being measured against a relevant benchmark and comparable peer set. This prevents false conclusions.

They validate:

Fees and total cost impact

Fees matter because they affect net outcomes and incentives. Institutions prefer fee structures that support long-term behaviour.

They assess:

For the fees of our Datt Absolute Return Fund and Datt Small Companies Fund, visit the respective Fund pages.

Most managers look good on paper during favourable markets. Qualitative due diligence tests what drives performance and whether the process can scale.

Investment philosophy and edge

Professional investors want a clear explanation of how the manager generates returns and why the edge should persist.

They test:

A credible investment manager in Australia can explain their philosophy in plain language and link it directly to real portfolio decisions.

Portfolio construction discipline

Portfolio construction is where risk becomes intentional. Professionals want evidence the manager controls exposures through design, not hope.

They assess:

Risk management and controls

Professional investors want to see risk as a system; they check whether controls are formal, monitored, and acted on consistently.

They review:

Team stability and key person risk

Investors allocate to teams, not individuals. A strategy dependent on one decision-maker increases business risk even if performance is strong.

They assess:

Governance, stewardship, and alignment

Governance is one of the strongest institutional filters. Strong returns do not offset weak alignment.

Investors check:

Transparency and reporting quality

Professional investors expect reporting that is specific, consistent, and testable.

They value:

Institutional investors usually reject managers due to structural risk, not one weak month.

The most common red flags include:

The best-performing manager in the last 12 months is often not the best long-term allocation. Professional investors avoid performance chasing because it increases timing risk.

They prioritise:

If you are assessing a fund manager in Australia, this framework helps you separate durable capability from temporary performance.

If you would like to learn more about Datt Capital’s investment philosophy or view our product offerings, please visit our website. You can also contact Daniel Liptak, Head of Distribution, on 0419 004 524 or email daniel@datt.com.au.

A repeatable process that delivers net outcomes across market cycles with controlled risk.

They assess both, but risk-adjusted returns and drawdowns often drive the final decision.

They test consistency, factor exposures, portfolio decisions, and the strength of the documented process.

Disciplined portfolio construction, robust risk controls, stable teams, and strong governance.

Fees reduce net outcomes and influence incentives. Investors want value-add that persists after costs.

Style drift, weak risk discipline, liquidity mismatch, key person dependency, and poor transparency.

Disclaimer: This article does not take into account your investment objectives, particular needs or financial situation; and should not be construed as advice in any way. The author may hold stocks discussed in this article. Forward-looking statements reflect the author's views at the time of writing and are subject to change. Past performance is not indicative of future results.

Investment Excellence with a Proven Edge

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2025. ALL RIGHTS RESERVED.

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2026. ALL RIGHTS RESERVED.

The information on this website is prepared and issued by Datt Capital Pty Ltd (ABN 37 124 330 865 AFSL 542100) (Datt Capital). Unless otherwise stated, the information is intended for wholesale clients within the meaning of section 761G or 761GA of the Corporations Act 2001 (Cth) (Corporations Act).

Datt Capital is the investment manager of the Datt Capital Absolute Return Fund (APIR FHT3309AU), the Datt Small Companies Fund Class A (APIR FHT4217AU), and the Datt Small Companies Fund Class B (APIR FHT4217AU) (together, the Funds). Fundhost Limited (ABN 69 092 517 087 AFSL 233045) (Fundhost) is the issuer and trustee of each Fund.

The Datt Capital Absolute Return Fund and the Datt Small Companies Fund Class A are available to wholesale investors only and must not be made available to any persons that are "retail clients" for the purpose of the Corporations Act. An investment in either of these Funds is available directly through a valid application form attached to the relevant information memorandum, through the Olivia123 direct application platform, or through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in either Fund you should consider the relevant information memorandum in full. The Datt Small Companies Fund Class B is available to retail investors only, exclusively through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in this Fund you should consider the relevant Product Disclosure Statement (PDS) in full. The PDS is available on request by contacting Datt Capital directly.

The information contained on this website or in any email is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Datt Capital or Fundhost to any registration or other requirement within such jurisdiction or country. Datt Capital may provide general information to help you understand our investment approach. Any financial advice we provide has not considered your personal circumstances and may not be suitable for you. To the extent permitted by law, Datt Capital and Fundhost, their officers, employees, consultants, advisers and authorised representatives, are not liable for any loss or damage arising as a result of any reliance placed on this document. Information has been obtained from sources believed to be reliable, but we do not represent it is accurate or complete, and it should not be relied upon as such. Datt Capital and Fundhost do not guarantee investment performance or distributions, and the value of your investment may rise or fall. Past performance is not an indicator of future performance.