ASX healthcare stocks have been repriced by sector degrossing, not weaker fundamentals. See where the valuation gap sits.

~ 3 min. read

By: Datt Capital

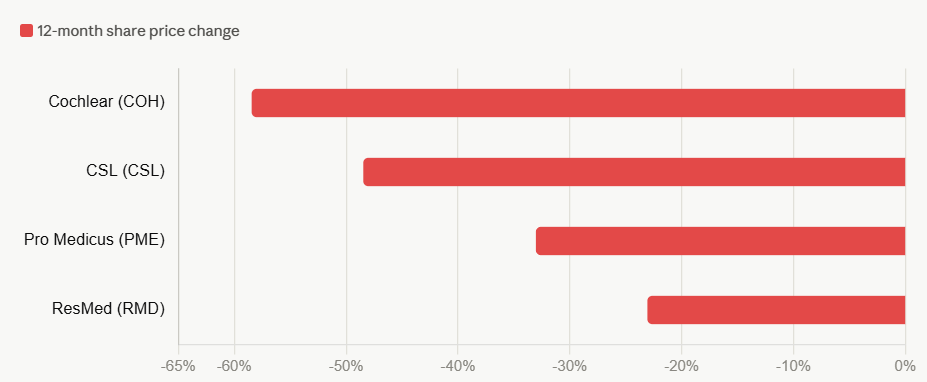

CSL has fallen by roughly half from its 52-week high. Cochlear is down well over half. Pro Medicus has dropped roughly a third from its peak. CSL, Cochlear and Pro Medicus rank among the largest, most established names on the ASX healthcare boards. The scale of their repricing says more about positioning than about business performance.

CSL, Cochlear, ResMed and Pro Medicus have all moved down over the past 12 months, though not by equal amounts. Cochlear has fallen the furthest, down well over half. CSL follows at roughly half, Pro Medicus at roughly a third, and ResMed at just under a quarter, the smallest decline of the four but still a meaningful de-rating. A single company missing on execution does not produce a synchronised decline across four businesses with different products, different customers and different growth profiles, even where the magnitude varies.

"Valuations across ASX healthcare leaders have reduced significantly off elevated prior levels. This has been a sector-wide phenomenon, not a reflection of business quality." - Emanuel Datt, Chief Investment Officer, Datt Capital, says

Healthcare carried some of the highest valuation multiples on the ASX through the growth-at-any-price cycle. Institutional positioning unwinds indiscriminately at that scale. Funds reduce exposure across the names they hold most, concentrating the selling in the largest, most liquid healthcare stocks first. Multiple compression follows, independent of any change in earnings, market share or clinical demand.

Sector degrossing extends beyond the large caps. As funds trim healthcare weightings, the reduction flows down to smaller, less liquid names in the same sector, which sell off further on lighter volume and less analyst coverage. The result is a widening dispersion between share price and underlying business performance the further down the market cap curve an investor looks.

"Smaller companies have sold off due to this sector degrossing, often more sharply than the fundamentals justify." - Emanuel notes

A valuation reset driven by positioning is a different signal to investors than a genuine fundamental downgrade tied to weaker earnings power or competitive position. CSL's plasma therapies franchise, Cochlear's implant market share, ResMed's sleep and breathing platform and Pro Medicus's enterprise imaging contracts have held up at a rate their share prices do not reflect. Balance sheet strength is one of the clearer ways to test that gap, since a business funding growth from a position of financial strength is better placed to absorb a valuation reset than one relying on market sentiment to stay afloat. Datt Capital has applied this same distinction before, highlighting that disciplined research shaped its response to a sentiment-driven sell-off in a healthcare holding that later recovered once the market re-assessed the business against the price.

Passive strategies track the index down when a sector is degrossed, regardless of whether the underlying businesses still meet the bar for inclusion. An active fund manager with a research-led process is positioned to distinguish a sector-wide valuation reset from a genuine change in business quality, then act on that distinction while capital continues flowing out of the sector. Datt Capital's Absolute Return Fund was ranked in the top 10 equity long-only funds for 2025, a result built on this kind of sector-agnostic, research-led positioning.

"Good opportunities may be found in unloved sectors. That is precisely where disciplined, research-led analysis earns its keep." - Emanuel says

For an investor assessing sector exposure, the current healthcare repricing raises a specific question: has anything changed at the business level, or has the price simply followed the flow of capital out of a previously crowded trade. That distinction determines whether a reduced healthcare weighting reflects a genuine risk-adjusted return or a missed valuation opportunity, and it sits at the centre of how a high conviction fund approaches sector positioning after a broad repricing event.

The scale and uniformity of the decline across CSL, Cochlear, ResMed and Pro Medicus points to sector-wide degrossing, a mechanical reset that has moved faster than any change in fundamentals. That gap between price and business quality is where the current opportunity in ASX healthcare stocks concentrates.

To learn more about Datt Capital's approach to distinguishing valuation resets from genuine risk, visit our Investment Philosophy page or contact our Distribution Manager, Daniel Liptak, at 0419 004 524 or by email at daniel@datt.com.au.

Disclaimer: This article does not take into account your investment objectives, particular needs or financial situation; and should not be construed as advice in any way. The author may hold stocks discussed in this article. Forward-looking statements reflect the author's views at the time of writing and are subject to change. Past performance is not indicative of future results.

Investment Excellence with a Proven Edge

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2025. ALL RIGHTS RESERVED.

Datt Capital Pty Ltd

ABN 37 124 330 865

AFSL 542100

390 St Kilda Rd, Melbourne VIC 3004

© COPYRIGHT 2026. ALL RIGHTS RESERVED.

The information on this website is prepared and issued by Datt Capital Pty Ltd (ABN 37 124 330 865 AFSL 542100) (Datt Capital). Unless otherwise stated, the information is intended for wholesale clients within the meaning of section 761G or 761GA of the Corporations Act 2001 (Cth) (Corporations Act).

Datt Capital is the investment manager of the Datt Capital Absolute Return Fund (APIR FHT3309AU), the Datt Small Companies Fund Class A (APIR FHT4217AU), and the Datt Small Companies Fund Class B (APIR FHT4217AU) (together, the Funds). Fundhost Limited (ABN 69 092 517 087 AFSL 233045) (Fundhost) is the issuer and trustee of each Fund.

The Datt Capital Absolute Return Fund and the Datt Small Companies Fund Class A are available to wholesale investors only and must not be made available to any persons that are "retail clients" for the purpose of the Corporations Act. An investment in either of these Funds is available directly through a valid application form attached to the relevant information memorandum, through the Olivia123 direct application platform, or through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in either Fund you should consider the relevant information memorandum in full. The Datt Small Companies Fund Class B is available to retail investors only, exclusively through selected investor directed portfolio service (IDPS) platforms. Before making any decision to make or hold any investment in this Fund you should consider the relevant Product Disclosure Statement (PDS) in full. The PDS is available on request by contacting Datt Capital directly.

The information contained on this website or in any email is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Datt Capital or Fundhost to any registration or other requirement within such jurisdiction or country. Datt Capital may provide general information to help you understand our investment approach. Any financial advice we provide has not considered your personal circumstances and may not be suitable for you. To the extent permitted by law, Datt Capital and Fundhost, their officers, employees, consultants, advisers and authorised representatives, are not liable for any loss or damage arising as a result of any reliance placed on this document. Information has been obtained from sources believed to be reliable, but we do not represent it is accurate or complete, and it should not be relied upon as such. Datt Capital and Fundhost do not guarantee investment performance or distributions, and the value of your investment may rise or fall. Past performance is not an indicator of future performance.